plan early — unless it has this special feature")

[ad_1]

Sally Anscombe | Moment | Getty Images

When saving for retirement, investing sooner typically boosts growth over time. But you can lose money by maxing out your 401(k) too early in the year — unless the plan has a special feature.

Most 401(k) plans offer an employer match, which uses a formula to deposit extra money into the account, based on your deferrals. Typically, you must contribute at least a certain percentage of income each paycheck to receive the year’s full employer match.

However, some 401(k) plans offer a “true-up,” or additional deposit of the remaining employer match, for employees who max out contributions before the end of the year.

More from Personal Finance:

Average 401(k) savings rates recently hit a record — here’s what experts suggest

Investor home purchases jump for the first time in two years

5 ways to maximize your vacation days

“It’s an awesome perk,” but not all 401(k) plans offer a true-up, said Tommy Lucas, a certified financial planner and enrolled agent at Moisand Fitzgerald Tamayo in Orlando, Florida.

To that point, roughly 67% of plans that offer matches more than annually had a true-up in 2022, according to the Plan Sponsor Council of America’s latest annual survey. It’s typically most common in bigger plans, experts say.

No true-up can be an ‘absolute nightmare’

When a 401(k) doesn’t have a true-up, “it’s an absolute nightmare” because employees can easily miss part of the company match, Lucas said.

For example, let’s say you’re under age 50, making $200,000 per year, and your company offers a 5% 401(k) match without a true-up.

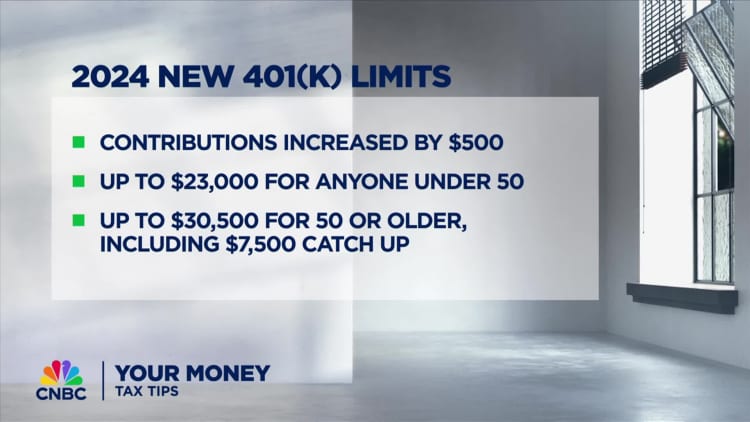

With 26 pay periods and a 20% contribution rate, you’ll reach the $23,000 employee deferral limit for 2024 after 15 paychecks and only receive about $5,800 of your employer match.

In this scenario, you’d miss about $4,200 of your remaining 5% employer match by maxing out the plan early, according to Lucas. That missed $4,200 could be worth tens of thousands more in future growth.

Typically, you can avoid the issue by equally spreading out contributions throughout the year, but you need to monitor changes, such as raises or bonuses, he said.

Review your summary plan description

Before setting your 401(k) deferrals, it’s important to know whether your plan has a true-up, experts say.

“That’s one of the things we investigate,” said CFP Dan Galli, owner of Daniel J. Galli & Associates in Norwell, Massachusetts.

Typically, the best place to look is the “contributions” section of your 401(k) summary plan description, which may or may not mention the feature, he said.

“It’s never going to say, ‘This plan does not have a true-up,'” Galli said. But you can double-check with your company’s human resources department to confirm, which may prompt the company to add a true-up feature in the future.

[ad_2]

Source link

{kind=link}