In my last article for London Wallet, I asked whether housing would be seen as an easy target for boosting tax receipts. That question seems to be answered. In August, both the Times and Guardian ran stories about options “Ministers were considering” around property taxation.

The headline proposal: abolishing stamp duty and replacing it with an annual property tax on homes worth over £500,000. Other mooted reforms included capital gains tax on homes over £1.5m and a council tax revaluation with new upper bands.

We don’t know what will happen, but something does need to change to get the market moving – boosting home moves, supporting economic growth, and expanding the revenue pool for estate agents.

Replacing stamp duty with an annual property tax

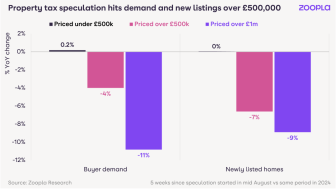

The prospect of replacing stamp duty with an annual levy grabbed attention and, unsurprisingly, created uncertainty. Our latest House Price Index shows a drop in higher-value buyer enquiries since the stories broke: -4% above £500,000 and -11% above £1m. New listings over £1m are down 9% as many of these buyers are also sellers.

There are still active buyers, but slightly fewer – so sellers will need to adjust their expectations.

On paper, scrapping stamp duty looks positive for the industry, particularly for the mass market. It lowers buying costs in the £250,000–£500,000 bracket, where many transactions occur, encouraging more moves.

The uncertainty is over what replaces it. For example, a £750,000 purchase could mean £4,000 in annual tax. After eight years, buyers would have paid as much as they would have in SDLT upfront, and over 20 years, far more. For homes under £500,000, however, buyers would save immediately – e.g. £5,000 less on a £300,000 purchase.

Estimated impact of annual property tax (Zoopla Research):

+ £300k home: saving of £5,000 (no annual tax)

+ £500k home: £2,700 per year; costs more after 6 years

+ £1m home: £8,180 per year; costs more after 5 years

+ £1.5m home: £12,270 per year; over 20 years, 10% of property value

What does this mean for prices and sales?

The key calculation for buyers is how long they’ll stay put. Recent movers average 8–9 years, but across all households the average is 20. Longer stays mean higher tax exposure – buyers may adjust what they’re willing to pay.

This implies downward price pressure on higher-value homes, particularly at £1m+. A £1.5m property, for example, would cost £151,650 more in tax over 20 years than SDLT upfront. With charges likely indexed to inflation, values would need to at least keep pace.

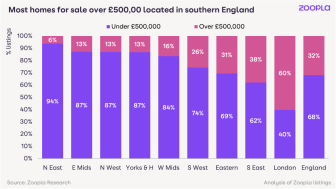

The impact would be felt most in southern England, where more properties sit above £500,000. Short-term, we should expect disruption as buyers and sellers process the changes.

Could reforms boost transactions?

One potential benefit is more frequent moves. Instead of staying in larger homes for decades, households might adjust more regularly to life changes to manage tax exposure. More liquidity would be positive for estate agents, offsetting some of the drag from downward price pressures.

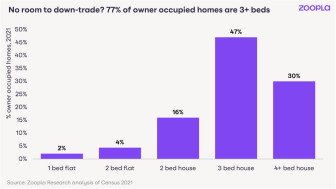

However, this relies on the availability of suitable homes. Three-quarters of UK private housing stock is 3+ bed houses. Smaller homes are relatively scarce, keeping two-bed prices close to three-beds and making “downsizing” less financially attractive. Without a greater supply of more smaller properties, many households could end up paying higher taxes without realistic options to reduce their liability.

Reform must be about market health, not plugging financial gaps

The case for reforming property tax is clear. Stamp duty acts as a brake on transactions, especially in higher-value markets. An annual levy could, in theory, encourage more moves and bring new energy to the market.

But the motivation should not simply be filling a hole in the public finances. Reform should be designed to boost market liquidity, support economic growth, and unlock more home building. Without parallel policies to expand supply, particularly of smaller homes, many households may feel penalised rather than empowered to move.

For now, uncertainty is the only certainty. With the Budget approaching, agents should prepare for continued disruption as sellers and buyers pause to see what reforms materialise. But the industry should also recognise that well-designed reform could deliver more frequent moves and, ultimately, more revenue opportunities for agents.

OPINION: With UK housing worth £10trn, is a tax hike inevitable?

{kind=link}